The ratio of lower-quality subprime mortgages originated rose from the historical 8% or lower range to approximately 20% from 2004-2006, with much higher ratios in some parts of the U.S. A high percentage of these subprime mortgages, over 90% in 2006 for example, were adjustable-rate mortgages. These two changes were part of a broader trend of lowered lending standards and higher-risk mortgage products. Further, U.S. households had become increasingly indebted, with the ratio of debt to disposable personal income rising from 77% in 1990 to 127% at the end of 2007, much of this increase mortgage-related.

Advanced

After U.S. house sales prices peaked in mid-2006 and began their steep decline forthwith, refinancing became more difficult. As adjustable-rate mortgages began to reset at higher interest rates (causing higher monthly payments), mortgage delinquencies soared. Securities backed with mortgages, including subprime mortgages, widely held by financial firms, lost most of their value. Global investors also drastically reduced purchases of mortgage-backed debt and other securities as part of a decline in the capacity and willingness of the private financial system to support lending. Concerns about the soundness of U.S. credit and financial markets led to tightening credit around the world and slowing economic growth in the U.S. and Europe.

hair dresses amortization

The immediate cause or trigger of the crisis was the bursting of the United States housing bubble which peaked in approximately 2005–2006. High default rates on "subprime" and adjustable rate mortgages (ARM), began to increase quickly thereafter. An increase in loan incentives such as easy initial terms and a long-term trend of rising housing prices had encouraged borrowers to assume difficult mortgages in the belief they would be able to quickly refinance at more favorable terms. Additionally, the economic incentives provided to the originators of subprime mortgages, along with outright fraud, increased the number of subprime mortgages provided to consumers who would have otherwise qualified for conforming loans. However, once interest rates began to rise and housing prices started to drop moderately in 2006–2007 in many parts of the U.S., refinancing became more difficult. Defaults and foreclosure activity increased dramatically as easy initial terms expired, home prices failed to go up as anticipated, and ARM interest rates reset higher. Falling prices also resulted in 23% of U.S. homes worth less than the mortgage loan by September 2010, providing a financial incentive for borrowers to enter foreclosure. The ongoing foreclosure epidemic, of which subprime loans are one part, that began in late 2006 in the U.S. continues to be a key factor in the global economic crisis, because it drains wealth from consumers and erodes the financial strength of banking institutions.

mortgage amortization table

1) Mortgage amortization table

1) Mortgage amortization table

QuikCalc Amortization Home

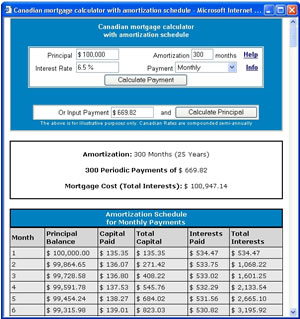

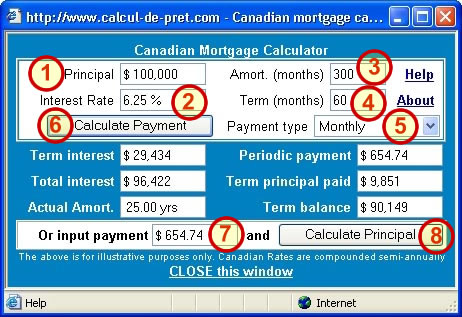

Canadian Mortgage Calculator

Mortgage Amortization Table

Canadian Mortgage Payments:

The Canadian Mortgage

Advanced

After U.S. house sales prices peaked in mid-2006 and began their steep decline forthwith, refinancing became more difficult. As adjustable-rate mortgages began to reset at higher interest rates (causing higher monthly payments), mortgage delinquencies soared. Securities backed with mortgages, including subprime mortgages, widely held by financial firms, lost most of their value. Global investors also drastically reduced purchases of mortgage-backed debt and other securities as part of a decline in the capacity and willingness of the private financial system to support lending. Concerns about the soundness of U.S. credit and financial markets led to tightening credit around the world and slowing economic growth in the U.S. and Europe.

hair dresses amortization

The immediate cause or trigger of the crisis was the bursting of the United States housing bubble which peaked in approximately 2005–2006. High default rates on "subprime" and adjustable rate mortgages (ARM), began to increase quickly thereafter. An increase in loan incentives such as easy initial terms and a long-term trend of rising housing prices had encouraged borrowers to assume difficult mortgages in the belief they would be able to quickly refinance at more favorable terms. Additionally, the economic incentives provided to the originators of subprime mortgages, along with outright fraud, increased the number of subprime mortgages provided to consumers who would have otherwise qualified for conforming loans. However, once interest rates began to rise and housing prices started to drop moderately in 2006–2007 in many parts of the U.S., refinancing became more difficult. Defaults and foreclosure activity increased dramatically as easy initial terms expired, home prices failed to go up as anticipated, and ARM interest rates reset higher. Falling prices also resulted in 23% of U.S. homes worth less than the mortgage loan by September 2010, providing a financial incentive for borrowers to enter foreclosure. The ongoing foreclosure epidemic, of which subprime loans are one part, that began in late 2006 in the U.S. continues to be a key factor in the global economic crisis, because it drains wealth from consumers and erodes the financial strength of banking institutions.

mortgage amortization table

1) Mortgage amortization table

1) Mortgage amortization table

QuikCalc Amortization Home

Canadian Mortgage Calculator

Mortgage Amortization Table

Canadian Mortgage Payments:

The Canadian Mortgage

No comments:

Post a Comment